Upcoming Event

Free Newsletter

Free Newsletter

Oil prices poised to increase

Contributing Writer //December 21, 2022//

The markets think they have seen signs of a slower pace of economic activity, evidence that the inflation rate has peaked and is headed lower, and have concluded that the Fed might actually be able to pull off the elusive soft landing. While the Fed also anticipates a soft landing, but only if the funds rate climbs from its current level of 4.4% to an expected peak of 5.1% in 2023.

In that case, the inflation rate will shrink to the desired 2.0% target pace — but not until the end of 2025! We believe that the Fed’s view is likely to be more accurate — it is going to be a long gradual process.

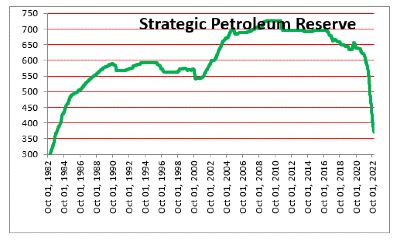

One reason that the inflation rate has fallen in recent months is because the Administration has chosen to release 180 million barrels of oil from the Strategic Petroleum Reserve. But that drawdown will be complete by the end of this month. The oil market will need to find the additional oil somewhere. As a result, oil prices seem likely to rise in the months ahead.

The Energy Information Agency expects crude prices to average $86.36 next year versus $73 currently, and gasoline prices to average $3.51 compared to $3.23. Those prices are some 10-15% higher than they are currently. That is not a lot, but the point should be that the downward bias to inflation since Biden chose to tap the Strategic Petroleum Reserve in March will soon disappear. While the overall inflation rate is likely to slow in 2023, it seems more likely to be a far more gradual downturn than the rapid drop that the market is expecting. Following a 5.8% increase this year we expect the core CPI to slow to 4.3% next year, and 2.5% in 2024.

The Strategic Petroleum Reserve was established in December 1975 in the wake of the Arab oil embargo which resulted in long gas lines. The idea was to have a stock of oil that would act as an insurance policy in the event of severe energy supply interruptions. The government then began to fill the reserve which reached a high point of 726 million barrels per day in 2010. There have been three emergency releases from the SPR — 34 million barrels in 1991 during Operation Desert Storm, 30 million barrels in 2005 following Hurricane Katrina, and 60 million barrels in 2011 following crude oil supply disruptions in Libya and other countries. While the current release was not declared an emergency, at 180 million barrels the release ordered in March dwarfed the size of any prior release.

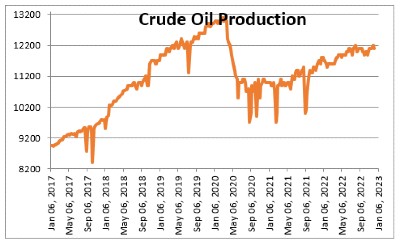

The current release was announced as 1 million barrels every day for six months. With current production of 12.1 million barrels per day the additional 1 million bpd from the SPR brought the total oil available to 13.1 million bpd which is roughly where production was prior to the recession. But now, missing the steady injection from the SPR, daily production will revert to 12.1 million bpd.

The current release was announced as 1 million barrels every day for six months. With current production of 12.1 million barrels per day the additional 1 million bpd from the SPR brought the total oil available to 13.1 million bpd which is roughly where production was prior to the recession. But now, missing the steady injection from the SPR, daily production will revert to 12.1 million bpd.

When the Administration announced the release back in March it said that “This record release will provide a historic amount of supply to serve as a bridge until the end of the year when domestic production ramps up.” The problem is that the EIA currently expects production to quicken only slightly from 12.1 million bpd currently to 12.3 million in 2023. If that is the case, it will not even come close to replacing the 1.0 million bpd currently available from the SPR. That seems to translate into higher oil prices ahead. The increase in crude prices may not be dramatic, to perhaps $85 per barrel, but the fact that oil prices are going up contrasts to the downward bias to inflation caused by falling oil prices since mid-year.

At the moment the market expects the funds rate to be 4.5% at the end of 2023. The Fed expects it to reach a peak of 5.1% in 2023. We look for it to be 6.0% by the end of 2023. What this suggests is that the markets seem to be priced for perfection. With oil prices on the rise, shelter prices climbing at a 7.1% pace, and a still very tight labor market causing upward pressure on wages, we suggest the market is being way too optimistic.

At the moment the market expects the funds rate to be 4.5% at the end of 2023. The Fed expects it to reach a peak of 5.1% in 2023. We look for it to be 6.0% by the end of 2023. What this suggests is that the markets seem to be priced for perfection. With oil prices on the rise, shelter prices climbing at a 7.1% pace, and a still very tight labor market causing upward pressure on wages, we suggest the market is being way too optimistic.

A separate question is whether the current size of the Strategic Petroleum Reserve is adequate. The president can pump the SPR at a maximum rate of 4.4 million barrels per day for 90 days. If he were to choose to do so, the current stock of 382 million barrels would be fully depleted by the end of the 90-day period. If he were to release it at a more gradual 1.0 million bpd pace as he did in 2022 the SPR would last about a year. In any emergency a drawdown of 1.0 million bpd will not go far. It seems likely that in that situation the current stock will be hard pressed to last more than 3-6 months. That, in our opinion, is inadequate. We need a much bigger insurance policy.

The Biden Administration has committed to replenishing the SPR when oil prices fall to or below $67-72 per barrel. Given that oil prices are $73 currently and poised to rise, the SPR is unlikely to be replenished any time soon.

From 1980 until 2003, when he retired, Stephen Slifer served as chief U.S. economist for Lehman Brothers in New York City, directing the firm’s U.S. economics group along with being responsible for forecasts and analysis of the U.S. economy. He has written two books on using economic indicators to forecast financial moves and previously served as a senior economist at the Board of Governors of the Federal Reserve in Washington, D.C. Slifer can be reached at www.numbernomics.com.